One of the reasons GPS can provide investors with above market returns is due to our operating a niche product (service, skill and culture are other reasons).

In general terms, GPS loans are too big for the bank manager but too small for their property departments.

When re-engineering the GPS business post-GFC, there were several items I wanted to enshrine into the GPS business model, such as:

1. We do senior debt, senior debt and only senior debt. We do not do second mortgages, mezzanine funding, joint ventures and the like.

2. We stick to our long-established and proven niche product.

3. It is all about looking after our investors’ best interests. The rest will follow from providing good service.

4. Not to become an institution. To stick to being a small and tightly run business.

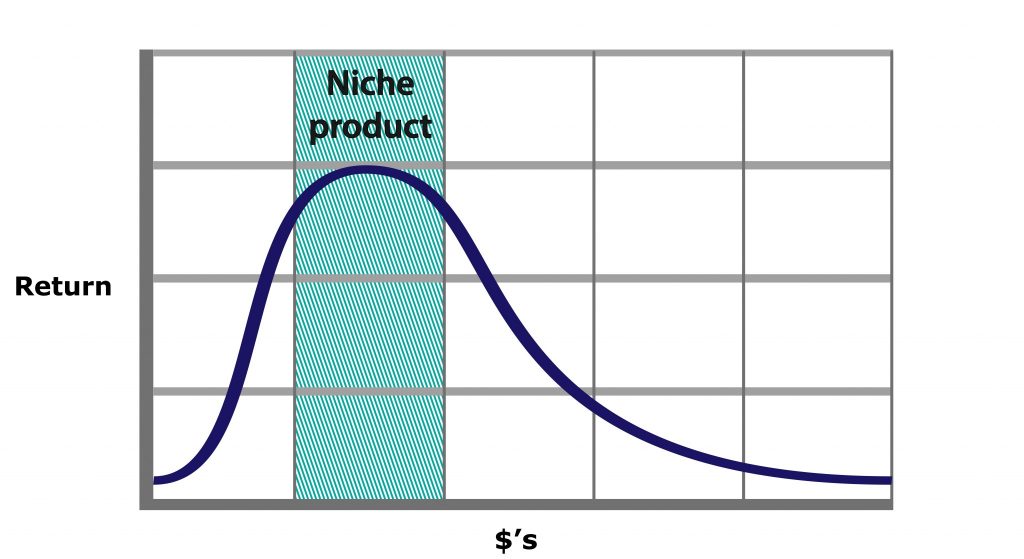

My initial study was on the viability of the business where I developed the following graph, which shows the income to GPS against funds under management.

What came out of the study is that if you do not have enough funds under management you cannot generate a consistent return with fixed overheads eating away at profit. Then came the strong return phase, which included overheads for a small but competent team that was not reliant upon one or two people. The graph then shows that as the business becomes larger and heading towards being an institution, the overhead costs and margin from lending reduced profitability.

I then looked at investors’ returns. The graph was quite similar, which means the best interests of investors and GPS coincide. When there is a smaller amount of funds under management a consistent return was not possible, as usage ratios were lower. Then came the strong return phase to investors, where there was consistent usage of funds under management. Returns to investors then starts to drop. The traditional GPS loan product and market only has a limited depth, and increasing lending past this point leads to either a lowering of quality of loans, or lending into more competitive markets. By the time you are at institution size you are doing home loans, as that is where the volume is in the Australian lending market. If you are lending money at around 4% to borrowers and want a margin, then investors are going to get very little return.

Another aspect was my personal knowledge of loans. When lending is only a small part of the overall business, it can be left to others. There is then the number of loans which my comprehension can absorb. As the number of loans increases beyond my capacity to comprehend, my knowledge of each loan declines.

Thanks to the loyal and long-established GPS investor base, we are now sitting in the “niche market” quadrant for funds under management.

I revisited my analysis work on this topic when reviewing the 2016 fund performance summary from another well-known mortgage fund. In five years, their funds under management has grown from approximately $450 million to approximately $1.1 billion, but returns on their pooled fund have gone from 7.65% to 5.23%. Distributions from the GPS Invest Pooled Fund have grown in this period to a very consistent 8.75% p.a. I think this proves my point. However, I am confident that the other well-known mortgage fund would not agree.